BMO Real Financial Progress Index: Nearly 8 in 10 Americans making big changes to holiday spending due to inflation, sharp decline in financial confidence

The latest BMO Real Financial Progress Index found that 77 percent of Americans said inflation is impacting their holiday spending decisions. The finding is part of a sharp drop in financial confidence this quarter, with of the number of U.S. adults who say they feel financially confident declining from 79 percent one year ago to 68 percent this quarter.

As Americans continue to feel the pinch of inflation on their finances, they reported turning to a variety of financial changes to offset the impact of an inflationary economic climate this holiday season. BMO’s survey found that 37 percent said they would purchase less expensive gifts, 30 percent will reduce big purchases, 27 percent will spread purchases over several months, and 29 percent will trim their gift recipient list to save money. Additionally, nearly half of Americans (45 percent) plan to purchase gifts using a credit card this year, despite credit card debt being a high source of anxiety (54 percent).

What’s more, 44 percent plan to modify or push back major purchases that they were planning to make this year, including 60 percent of Americans who no longer intend to move forward on buying a car or home. Younger Americans reported being more likely to rely on their savings and buy now, pay later (BNPL) programs to pay for this year’s holiday gifts.

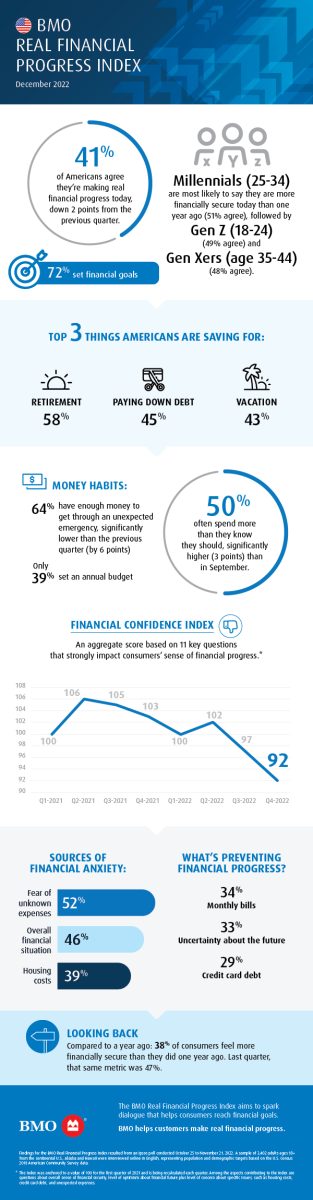

Aside from holiday spending, as paying down debt becomes significantly more important, retirement savings and vacation funds are being deprioritized. In fact, nearly half (45 percent) of Americans report paying down debt as one of their financial goals, up significantly from last quarter (39 percent). Meanwhile, Americans who report saving for retirement dropped from 62 perfect last quarter to 58 percent this quarter, while those saving for vacation dropped from 48 percent to 43 percent.

Financial Anxiety Remains High

A large majority of Americans (83 percent) said their financial situation has caused them increased anxiety. The most significant sources of financial anxiety, according to the survey, include fear of unknown expenses (85 percent), family-related expenses (69 percent), housing costs (68 percent). Additionally, Americans reported that credit card debt (54 percent) is causing them financial anxiety.

In addition to the top causes of financial anxiety, Americans also report the following:

- 67 percent of Americans said medical bills are causing their financial anxiety with 74 percent of those aged 25 to 34 reporting they are struggling to pay medical bills, up seven points from last quarter.

- 63 percent of Americans aged 55 to 65 report that keeping up with monthly bills is causing them financial anxiety, rising 16 percent from last quarter.

“Inflation’s impact on American’s finances is evident and it is having a direct impact on how people shop this holiday season as well as their 2023 budget planning,” said Paul Dilda, Head of U.S. Consumer Strategy at BMO. “In addition to setting and following a holiday budget this year, it is crucial for Americans to create a financial plan for 2023, especially during a cycle of high inflation like we are experiencing now. As we head into the new year, a key to alleviating financial anxiety will be learning how to protect financial progress you have made already, and how to continue tackling debt to make progress through a challenging economy.”

Outlook for 2023

Looking ahead to the new year, 44 percent of Americans said their financial resolutions have changed due to inflation, with younger Americans (60 percent) aged 25-34 reporting that their resolutions have changed compared to just 22 percent of those over the age of 65. Minimizing spending was reported as a top goal (31 percent), followed by creating a budget (19 percent).

Additionally, about two thirds of adults (66 percent) plan to buy, sell or refinance a home in 2023.

“Now is the time for Americans to take control of their finances,” said Tina DeGustino, Director of Consumer Strategy at BMO. “Several steps can be taken to achieve this today, such as evaluating monthly budgets in relation to the higher cost of everyday items and adjusting spending habits accordingly, strongly committing to savings and retirement goals, and setting aside time for frequent check-ins or scheduling time with your banker. These steps will help ensure a steady financial course and are crucial to meeting long-term financial goals.”

In addition to creating a holiday spending budget and sticking to it, BMO offers the following tips to help Americans make real financial progress and navigate inflation as the new year approaches:

- Use free digital banking tools and apps to help track spending patterns and save.

- Take advantage of BMO’s free financial literacy e-book that addresses key financial topics such as budgeting, debt and credit management, digital banking, homeownership, loans and retirement planning.

- Make a budget or savings plan for large purchases like a car, vacation, or new appliance.

- When evaluating what you owe, pay down debt with the highest interest rate first.

- When possible, look to consolidate debt with the many vehicles available, such as utilizing the equity in your home or your taxable investments as collateral to potentially get a loan with a lower interest rate.

- Evaluate big household expenditures, such as Property Causality Insurance, and work with your financial advisor to search for quotes with qualified carriers to see if you can improve upon coverage and save money.

- Link your checking and savings accounts to have a clear view of what you are spending and saving.

- Take advantage of 0 percent credit card offers which allow you to borrow money for a limited time without accruing interest or transfer the balance from a high-interest credit card to a 0 percent interest card to help pay down the balance quicker.

- Assess ongoing expenses such as streaming services, cable and internet plans, gym memberships or phone providers and negotiate lower prices when possible or work to reduce or eliminate programs you don’t use often.

- Speak with an expert to make sure your savings and payment patterns are on track to reach both near- and long-term goals and that you have the right financial tools in your toolbelt to achieve goals, such as buying a house or car, or improving your credit score.

To find out how BMO can help customers make financial progress, visit: https://www.bmoharris.com/main/personal

About the BMO Real Financial Progress Index

Launched in February 2021, the BMO Real Financial Progress Index is an indicator of how consumers feel about their personal finances and whether they are making financial progress. The index aims to spark dialogue that will help consumers reach their financial goals and to humanize a topic that causes anxiety for many – money.

The research detailed in this document was conducted by Ipsos in the United States from October 24 to November 28, 2022. A sample of n=3,402 adults ages 18+ in the US were collected. Quotas and weighting were used to ensure the sample’s composition reflects that of the U.S. population according to census parameters.